The Federal Open Market Committee (FOMC) left its benchmark interest rate unchanged at 4.25%–4.50% at its July 29–30 meeting. The decision reflects a balancing act: inflation remains somewhat elevated, boosted by tariff-driven increases in goods prices, while economic growth shows signs of fatigue and consumer spending softens.

Two members dissented, favoring a 25-basis-point cut, underscoring a growing split within the Committee about whether risks to employment are now outweighing upside risks to inflation.

Fed’s Assessment

-

Inflation: Headline PCE inflation held near 2.5%, with core at 2.7%. Tariffs are adding pressure to goods inflation, though services disinflation continues. The Fed remains divided over whether tariffs represent a one-time shock or a longer-lasting driver of price pressures.

-

Growth: GDP grew modestly in the second quarter after contracting in Q1. Consumption slowed, housing demand softened, and business investment was subdued. Trade flows remain volatile as companies front-load imports in anticipation of tariffs.

-

Labor Market: Unemployment ticked down to 4.1%, still near full employment. Wage growth moderated to 3.7% year-over-year, while firms reported cautious hiring due to policy uncertainty.

-

Markets: Equity prices climbed further, with valuations in the S&P 500 driven by optimism around large-cap technology firms benefiting from AI adoption. Small-caps, by contrast, remain below historical averages. Credit spreads narrowed to tight levels, but small business credit demand and supply remain subdued.

Implications for Financial Markets

Rates and Fixed Income

The Fed’s decision signals stability at the front end of the curve but leaves the door open to movement in either direction later this year. Quantitative tightening and higher Treasury issuance are expected to push reserves lower, supporting term premia. Investors should expect episodes of money-market stress around quarter-ends, tax dates, and settlement days.

Equities

Mega-cap tech continues to drive indices higher, with valuations stretched on AI optimism. While secular growth themes remain intact, these names are highly sensitive to interest rates and broader risk sentiment. Small-caps offer relative value but need stronger credit availability and growth momentum to close the performance gap.

Credit

Investment-grade and high-yield spreads remain historically tight, offering carry but limited protection if growth deteriorates. Corporates maintain strong market access, though small businesses are feeling the pinch of tighter credit standards. Private credit continues to expand, with insurers increasing exposure, but leverage and rollover risks are building.

Currencies and Commodities

The dollar has weakened slightly but remains range-bound, with tariffs and relative growth driving direction. Commodities are mixed: tariff-driven inflation supports gold and hard assets, while slowing demand tempers industrial metals and energy.

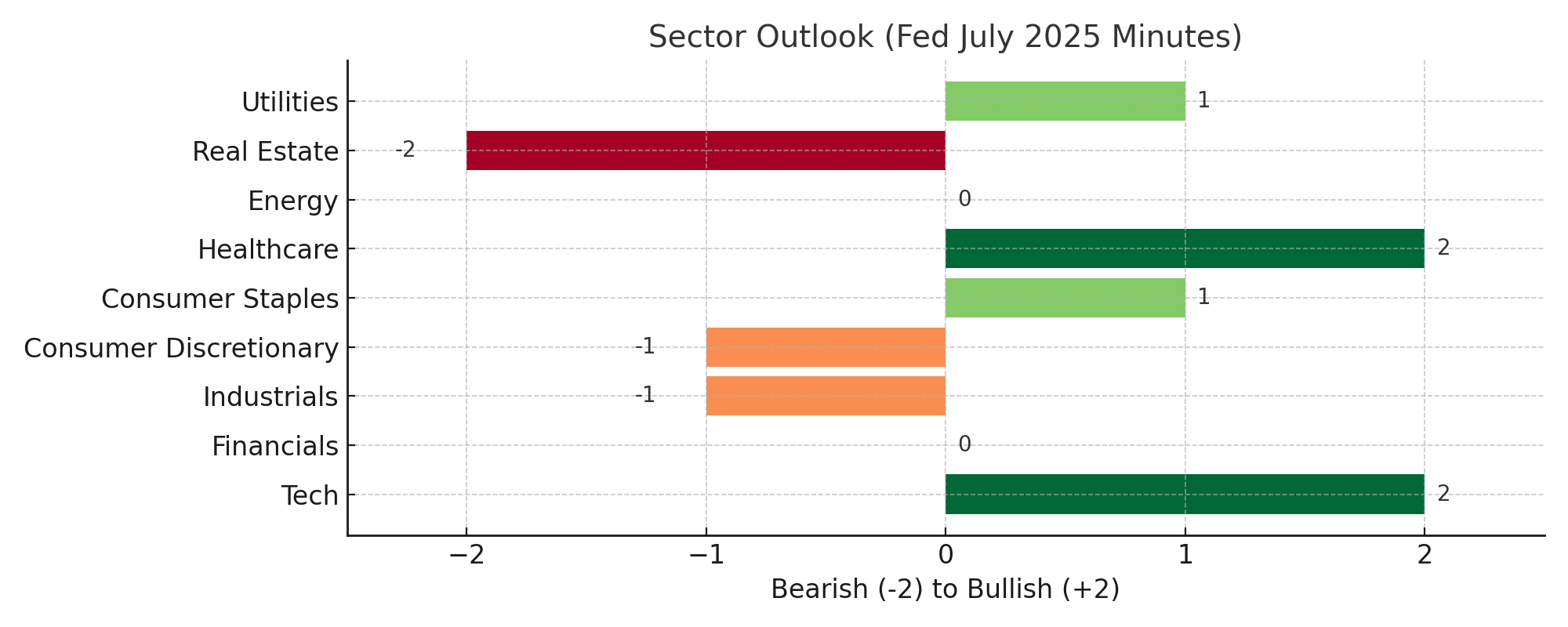

Sector Impacts

-

Technology: AI-driven leaders benefit from secular demand, though stretched multiples increase vulnerability to rate-driven volatility. Hardware and semiconductors face input-cost risks from tariffs.

-

Financials: Banks remain capital-strong but sensitive to long-end yield increases, which could deepen unrealized losses. Insurers’ growing reliance on private credit raises liquidity concerns. Asset managers benefit from issuance and tight spreads.

-

Industrials & Materials: Tariff pass-through remains uneven. Companies with flexible supply chains and automation investments are better positioned to protect margins.

-

Consumer Discretionary: Slower income growth and weaker housing weigh on spending, especially for big-ticket items. Value-focused retailers and companies with elastic pricing stand to fare better.

-

Consumer Staples: Defensive positioning and pricing power provide insulation from cost pressures.

-

Healthcare: A defensive growth sector with stable cash flows and limited tariff exposure.

-

Energy: Tariff-related inflation supports pricing, but weaker global growth caps upside. Integrated majors with disciplined capital allocation are favored.

-

Real Estate: High mortgage rates and falling housing demand weigh on housing-linked REITs, though logistics and data centers remain supported by structural trends.

-

Payments & Fintech: Stablecoin adoption may accelerate following new legislation, boosting Treasury demand but disrupting traditional banking channels.

Scenario Framework

-

Base Case: Tariff impact fades over time, inflation gradually moderates, and growth remains sluggish but avoids recession. The Fed holds rates before pivoting in 2026. This favors quality equities, investment-grade credit, and a modest steepening of the curve.

-

Sticky Inflation: Tariff costs persist, expectations drift upward, and the Fed keeps policy restrictive for longer. Value sectors, gold, and the dollar benefit. High valuations in growth equities become more vulnerable.

-

Growth Shock: Labor market softens more quickly, consumption slows sharply, and housing weakens. The Fed cuts sooner. Treasuries, defensive equities, and healthcare outperform, while high-yield credit spreads widen.

Investor Positioning

The Fed remains deliberately patient. Inflation is still above target, but much of the pressure comes from tariffs, which may prove temporary. Growth and employment risks are rising, but not yet decisive enough to shift policy.

For investors, this means markets remain supported by carry trades, strong liquidity in large-cap tech, and credit availability for larger corporates. Yet the cushion is thinner: credit spreads are tight, valuations are stretched, and liquidity risks in money markets are growing.

Key strategies:

-

Emphasize quality equities with balance-sheet strength and pricing power.

-

Maintain duration optionality in portfolios to hedge against growth risks.

-

Position for dispersion in credit and equities rather than broad beta exposure.

-

Keep defensives and real assets in focus as tariff-driven inflation lingers.

Bottom Line

The Fed is threading a narrow path: too aggressive on inflation, and growth risks rise; too quick to ease, and inflation expectations may unanchor. Investors should expect continued volatility around data releases, with the balance of risks tilted toward more selective opportunities across sectors.