The August jobs report delivered a significant surprise that has immediate implications for investors’ portfolios and Federal Reserve policy. Here’s what the data means for your investment strategy.

The Numbers That Matter

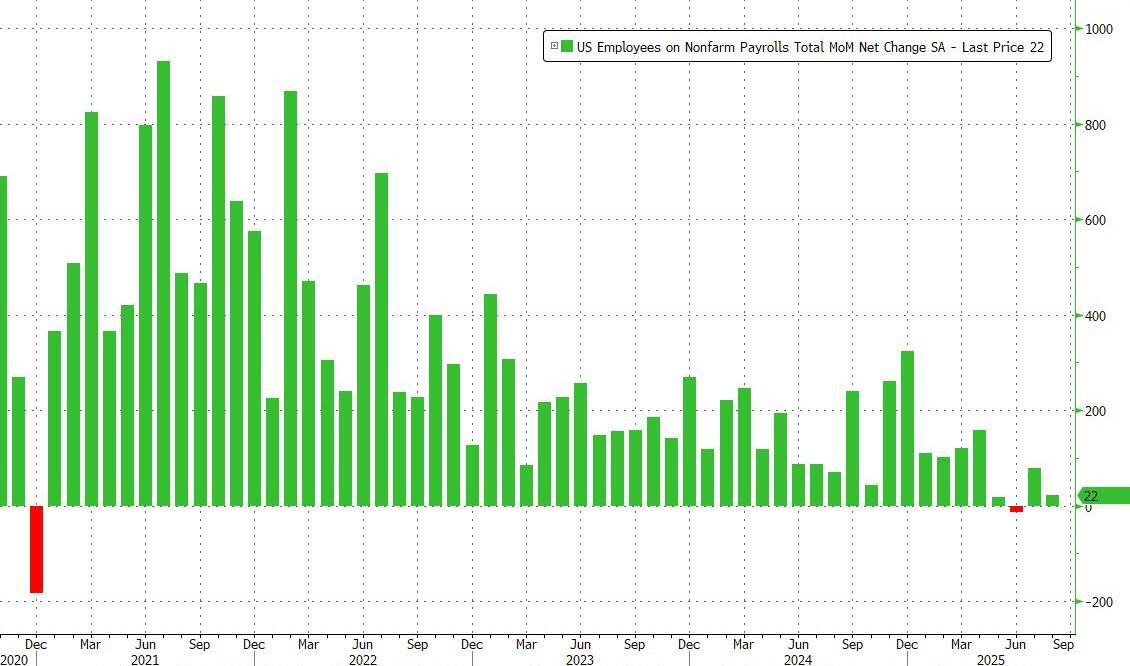

Job Creation Falls Short: The U.S. economy added only 22,000 jobs in August, dramatically below the 75,000 Wall Street consensus. This represents a concerning slowdown from July’s revised 79,000 jobs added.

Unemployment Rises: The unemployment rate climbed to 4.3% from 4.2%, with broader underemployment (U-6) reaching 8.1% – the highest level since October 2021.

Wage Growth Cools: Average hourly earnings increased 3.7% year-over-year, down from 3.9% in July, suggesting reduced inflationary pressure from wages.

What’s Behind the Weakness

The report reveals several troubling trends that investors should monitor:

Full-Time Jobs Disappearing: Full-time employment dropped by 357,000 positions for the second consecutive month, while part-time jobs surged by 597,000 – indicating employers may be cutting hours rather than hiring.

Multiple Job Holders Surge: Americans holding multiple jobs increased by 443,000, the largest monthly jump since the pandemic, suggesting people are taking additional work to make ends meet.

Revisions Paint Darker Picture: June’s job growth was revised from positive 27,000 to negative 13,000, marking the first negative monthly reading since 2020.

Investment Implications

Federal Reserve Response: The weak data significantly increases the probability of a 50 basis point rate cut at the Fed’s September meeting, rather than the previously expected 25 basis points. Lower interest rates typically benefit:

- Growth stocks and technology companies

- Real Estate Investment Trusts (REITs)

- Interest-sensitive sectors like utilities

Sector Analysis:

- Healthcare remained resilient, adding 31,000 jobs

- Federal government and energy sectors showed weakness

- Manufacturing continues declining, down 78,000 jobs over the past year

Market Positioning: The data suggests investors should consider:

- Defensive positioning as economic growth may be slowing

- Interest rate-sensitive investments that benefit from potential Fed cuts

- Companies with strong balance sheets that can weather economic uncertainty

The Bigger Picture

This jobs report confirms what many economists have suspected: the labor market is cooling faster than expected. The combination of slowing job growth, rising unemployment, and increased part-time employment suggests the economy may be entering a more challenging phase.

For investors, this creates both risks and opportunities. While economic weakness is concerning for corporate earnings, the likely Fed response of more aggressive rate cuts could provide support for equity valuations, particularly in interest-sensitive sectors.

Scenario Analysis: Three Potential Outcomes

Base Case (60% Probability): Soft Landing with Aggressive Easing

Fed Response: 50bp cut in September, followed by 25bp cuts at subsequent meetings Market Impact:

- Equity markets rally 5-8% by year-end, led by growth and rate-sensitive sectors

- 10-year Treasury yields fall to 3.5-3.8% range

- Dollar weakens 3-5% against major currencies Investment Strategy: Moderate risk-on positioning with emphasis on quality growth and REITs

Recession Scenario (30% Probability): Economic Contraction

Fed Response: 75bp emergency cut, followed by rapid easing cycle Market Impact:

- Equity markets decline 10-15% initially before Fed response rally

- Treasury yields fall below 3% as recession fears dominate

- Credit spreads widen significantly Investment Strategy: Maximum defensive positioning, focus on Treasuries, healthcare, and essential services

Stagflation Risk (10% Probability): Persistent Inflation with Slow Growth

Fed Response: Limited easing due to inflation concerns Market Impact:

- Equity markets remain volatile with sector rotation

- Real yields stay elevated

- Commodities and inflation-protected securities outperform Investment Strategy: TIPS, commodity exposure, and companies with pricing power

Long-Term Structural Implications

Labor Market Evolution: The shift toward part-time employment and multiple job holdings may reflect structural changes in the economy:

- Gig Economy Growth: Traditional employment relationships continue evolving

- Automation Impact: Technology displacement may be accelerating

- Skills Mismatch: Educational and training programs may need significant updates

Policy Implications: Employment weakness may influence:

- Fiscal Policy: Potential for increased government spending on job creation programs

- Immigration Policy: Labor shortage areas may require policy adjustments

- Education Policy: Skills training and retraining programs likely to gain political support

Investment Implementation Guide

Immediate Actions (Next 30 Days)

- Reduce cyclical exposure: Trim positions in manufacturing, discretionary retail, and regional banks

- Increase duration: Add long-term Treasury exposure for rate cut beneficiaries

- Defensive sector allocation: Increase healthcare, utilities, and consumer staples weightings

- Volatility hedging: Consider modest VIX or put option positions for portfolio protection

Medium-Term Positioning (3-6 Months)

- International diversification: Add developed and emerging market exposure

- Real estate allocation: Increase REIT exposure, focusing on residential and healthcare properties

- Credit positioning: Move up in credit quality while maintaining yield exposure

- Technology selection: Focus on established growth companies with strong balance sheets

Long-Term Strategic Considerations (6-12 Months)

- Structural theme investing: Healthcare innovation, renewable energy transition, and automation beneficiaries

- Currency hedging decisions: Evaluate dollar exposure in international investments

- Alternative investments: Consider private credit, infrastructure, and other diversifying strategies

- Tax optimization: Plan for potential capital gains realization before year-end

Bottom Line: Action Required

The August jobs report represents a fundamental shift in the economic and investment landscape. This isn’t merely a disappointing data point—it’s a potential inflection point that demands immediate portfolio reassessment.

Key Takeaways for Investors:

- Employment weakness is broad-based and accelerating, not confined to specific sectors

- Federal Reserve policy response will likely be more aggressive than previously expected

- Defensive positioning should be prioritized while maintaining exposure to rate cut beneficiaries

- International diversification becomes more important as U.S. economic risks rise

- Quality metrics matter more than ever as economic uncertainty increases

Immediate Action Items:

- Review portfolio cyclical exposure and consider reductions

- Increase defensive sector allocations (healthcare, utilities, consumer staples)

- Add duration through Treasury bond exposure

- Consider international diversification opportunities

- Implement appropriate hedging for downside protection

The convergence of employment weakness, potential Fed easing, and market repricing creates both significant risks and compelling opportunities. Investors who act decisively to reposition portfolios for this new environment will be best positioned to navigate the challenges and capitalize on the opportunities ahead.